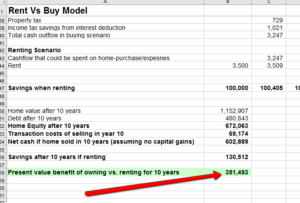

Just click the image below and you can download our custom rent vs buy excel calculator. When you use this calculator you can take a close look at the cost/benefit of renting vs buying in the Bay Area. People who downloaded this sheet were also interested in this buyers crash course. DOWNLOAD THE XLS FILE […]

Fast Bay Area Mortgage Loan Pre Approval

May 17, 2018 By 2 Comments

It’s so easy to get a mortgage pre-approval letter. It should only take about 15 minutes on the phone with a good Loan Officer and just a bit of work gathering a few income documents. We specialize in getting you pre approved fast in cities like Pleasant Hill, Walnut Creek, Concord, Martinez and Lafayette, or […]

MASTERCLASS: How to Scale your Business Idea This Year

May 13, 2018 By 2 Comments

How can you have a six figure year this year on the internet? Join our next live masterclass with Jason Wheeler hosting Chris Record and start exploding your business online using Google and Facebook. We’ll show you how. By now you likely know I am a huge advocate of marketing and advertising online. It’s how I’ve […]

(BPMI) Borrower Paid Mortgage Insurance vs (LPMI) Lender Paid

February 9, 2018 By 1 Comment

Mortgage insurance and the different types of requirements for the different policy options can prompt a lot of questions for potential home buyers. When you learn you need mortgage insurance it can be discouraging since it will often add to your over all costs for closing. In a nutshell… If you are purchasing a home […]

[CASE STUDY] 10 Day Mortgage Closings on a Home Purchase?

December 22, 2017 By 4 Comments

2019 HOME LOAN PURCHASE CLOSED IN JUST 12 DAYS In this most recent case study we closed this purchase loan in just 12 days!! The loan was submitted on August 28th 2019 and we had closing docs ready on 9/11/2019 We closed this purchase loan in only 10 days! In this recent case study I […]

How I Got BACK at Spam Callers While Getting a Good Laugh

October 19, 2017 By Leave a Comment

A couple weeks ago I was building out a new website and without me knowing it… my contact information was public and being sold to telemarketers on the new domain I had purchased… I accidentally got myself on a call list that I didn’t really want to be on. Next thing you know I have […]

6 Reasons It’s a Good Idea to Look at a Refinance

October 16, 2017 By 1 Comment

Paying a mortgage can feel like a trap sometimes! It feels like mortgage companies are sticking it to you right? Whether you recently bought a home two or three years ago, or if you’ve been paying on your current mortgage for several years there’s one thing that is certain. Mortgage servicer’s are interested in one […]

[5 Bonuses] Buy, Refi or Sell In The East Bay Area

September 19, 2017 By 1 Comment

Thank you for visiting my personal Real Estate and Lending blog. I truly appreciate it. I have an important message for you if you are thinking of buying or own Real Estate in the CA East Bay Area. Even if you are currently renting but maybe you are TIRED of the high rent costs here […]

Bay Area Sales Slow Mortgage Rates Hit 6 Month Lows

August 29, 2017 By Leave a Comment

Bay Area Real Estate costs are changing and changing quickly. Mortgage Rates have as of late dropped to a half year 2017 low. In this video I will show you… Mortgage Rate trend charts, Real Estate Market Reports for my main market (you can set up your own report if you want) A GREAT OPPORTUNITY […]

Special Home Loans For Bay Area Veterans With No Down Payment

August 15, 2017 By Leave a Comment

VETERANS HOME LOANS IN THE BAY AREA Are you a veteran that recently serve your country and struggling to make payments on your rent. Are you aware of it as a Veteran of the Navy Coast Guard Marines army or any other arm for service you were entitled to some of the best loan programs […]

Bay Area Lowest Down Payment Options to Buy A Home

August 15, 2017 By Leave a Comment

HOW MUCH DO I NEED FOR A DOWN PAYMENT IN THE BAY AREA? What is the lowest down payment option when it comes to purchasing a home here in the California bay area? The common misconception is that a down payment on a bay area house purchase could often buy you an entire house in […]

Bay Area Stated Income Jumbo Financing? Diablo Valley Luxury

May 24, 2017 By Leave a Comment

These stated income loans in the California Bay Area go up to 5 million 80% LTV as little as 20% down payment. No tax returns, no W2s or pay stubs needed. Send us your scenario. WHO CAN QUALIFY FOR STATED INCOME PROGRAM? This Bay Area Stated Income Loan program is specifically intended for people in […]

119 Ascot Court #1 Moraga CA Condo for Sale

May 22, 2017 By Leave a Comment

Open this Saturday and Sunday from 1:30 to 3:30pm SEE ALL DETAILS HERE Rare opportunity in the City of Moraga CA. Granite counter tops. Elegant bathrooms. Living room w/fireplace. New carpet. Unique backyard views. Top schools. Close to shopping & entertainment and recreation area. Move in & enjoy! 3 bedroom 2 1/2 bathrooms with 1,320 […]

264 AUGUSTINE, MARTINEZ CA 94553

April 1, 2017 By Leave a Comment

CLICK HERE FOR ALL OF THE PICTURES AND PROPERTY DETAILS The original listing price for this home was $797,000… Make a guess how much it sold for and you can win a $50 Amazon Gift Card or Venmo Cash. 264 Augustine is set at the end of a Cul De Sac. Pleasant Hill Schools Open […]

Thinking of Buying in 2019?

March 7, 2017 By 1 Comment

Here is the latest on East Bay Area Down Payment Options. Look over my shoulder, as I compare low down payment options to our zero down payment option that many home buyers are getting approved for recently. In this quick 10 minute video, I will show you a real life scenario comparison between two popular […]

Bay Area Reverse Mortgages

February 23, 2017 By Leave a Comment

Seniors all around Pleasant Hill are taking control of their finances without giving away their lifestyle. Did you know that the home equity conversion mortgage that is federally insured can help you purchase a home with no monthly payments, or refinance your current home with no monthly payments, if you are 62 and older. Many […]

5 Bonus Treasures for VIP Clients

February 14, 2017 By 2 Comments

Every week I work hard to bring you content full of value. I want you to test drive this content once per week. Every Tuesday I release the BEST content for those that are following and keeping up with the Bay Area Real Estate Market. If you hate it please tell me how to improve […]

I Just Posted This Recent Mortgage Article

January 22, 2017 By Leave a Comment

Here is the latest on Mortgages. Rates, trends, programs and things and important upcoming economic data. CLICK HERE TO READ THE FULL UPDATE I just poshttps://www.jasonwheeler.biz/wp-admin/post.php?post=5296&action=editted this recent mortgage update https://t.co/iPj7WCRwxd pic.twitter.com/bQBS9Ee7sI — Jason Wheeler (@JasonWheeler) January 23, 2017

Bay Area Home Prices Rising Or Falling?

December 8, 2016 By Leave a Comment

HOME PRICES FALLING OR INCREASING WITH MORTGAGE RATES? Are Bay Area home prices going to continue increasing or will they begin falling in 2017? Today, in this quick video, I wanted to hang out with you for just a few minutes and talk a little bit about the direction of mortgage rates since the election […]

WHY I OWE YOU BIG TIME & 4 THINGS I’M THANKFUL FOR

November 29, 2016 By Leave a Comment

If you’re anything like me, then you probably spend a lot of time between Thanksgiving and the end of the year reflecting on your previous year goal setting. During this time, I like to look at the successes that I created, the failures that I had, challenges that I overcame, and also challenges and hardships […]